condo document review Calgary

The Risks of Reviewing Calgary Condo Documents Yourself

Reading the documents is easy. Interpreting them correctly before your Calgary condition deadline is where most buyers get burned. Here is what DIY reviewers miss, and what it costs.

Leanna Vinogradov

Leanna Vinogradov

With a professional condo document review costing a few hundred dollars, it is tempting to save the money and read the documents yourself. After all, how hard can it be?

The honest answer: reading the documents is easy. Interpreting them correctly, under a deadline, is where most buyers get into trouble. If you have just accepted an offer, our guide to what to do during the Calgary condition period maps the full timeline. Here is what is actually in a condo document package, the costly things that are easy to miss, and how to decide whether to go it alone.

What is in a condo document package

In Alberta, a typical package can run to hundreds of pages and includes:

- Financial statements and the operating budget

- The reserve fund study and reserve fund plan

- Board and annual general meeting minutes, often spanning multiple years

- Bylaws, rules, and policies

- The insurance certificate and appraisal

- Engineering or technical reports, if any exist

Each document tells part of the story. The risk hides in how they fit together, and that is exactly what is hard to see when you are reading them for the first time.

The costly things DIY reviewers miss

1. An underfunded reserve fund

The reserve fund study lays out a plan for major repairs over decades. The crucial question is not whether the fund has money in it. It is whether the balance matches what the study says it should have at this point in the plan.

A fund that is far behind schedule is a flashing warning sign for a future special levy, and it is easy to overlook if you do not know what "adequate" looks like for a building of that age, size, and construction type.

2. Early signals of a special assessment

Special levies rarely appear out of nowhere. They are usually foreshadowed in the meeting minutes: repeated discussion of a leaking roof, failing windows, parkade repairs, or an insurance claim that never gets resolved. Spotting a recurring, unfunded problem across two or three years of minutes takes patient, trained reading, and it is the single most valuable thing a good reviewer does.

3. Restrictive bylaws

Bylaws can limit rentals, restrict pets, ban short-term stays, or impose age restrictions. A buyer who plans to rent the unit or bring a dog can be blindsided by a rule they skimmed past at midnight before a deadline.

4. Insurance gaps and deductibles

Condo corporation insurance often carries large deductibles, sometimes tens of thousands of dollars, that can be passed on to an owner responsible for a loss. Understanding what the policy does and does not cover requires reading the certificate carefully and knowing what to compare it against.

Reserve fund studies are brutally hard to read

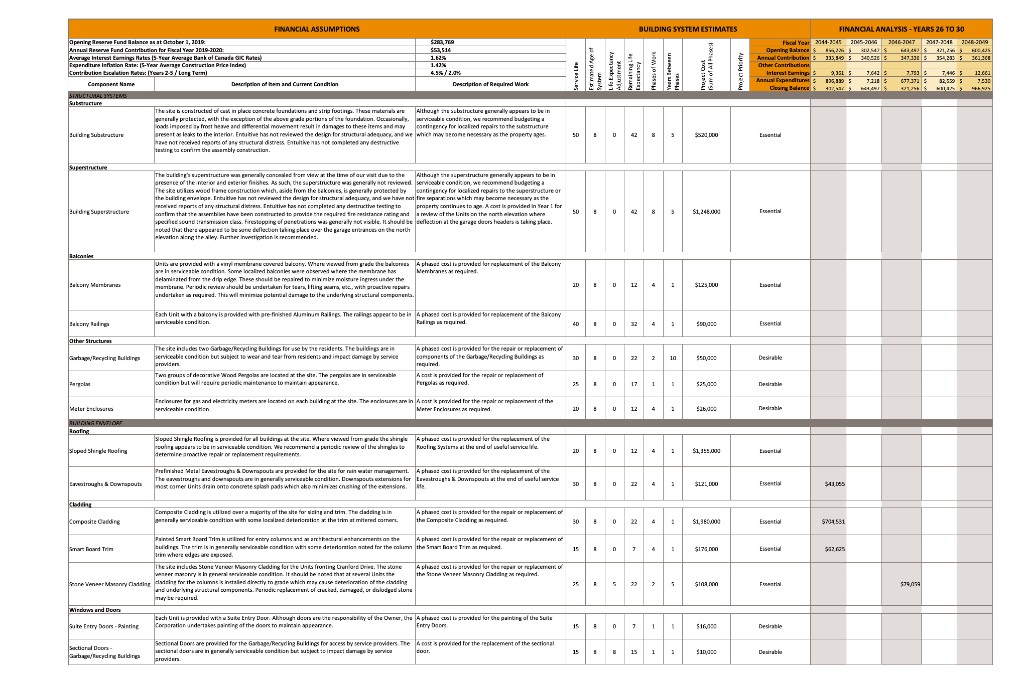

Of all the documents in the package, the reserve fund study is the most important and the hardest to interpret. People assume it boils down to a single question: is the fund "fully funded" or not? It is not that simple. A reserve fund study is a 30-year financial projection covering dozens of building components, each with its own service life, effective age, replacement cost, inflation assumption, and repair phasing.

Here is one slice of a real reserve fund study, showing just a handful of components over a five-year window:

Look at everything packed into that table. Every building system, from the substructure and superstructure to balconies, roofing, cladding, and doors, gets its own row with a service life, an effective age, a life-expectancy adjustment, the number of phases of work, the years between phases, a projected cost, and a priority rating. Across the top sit the financial assumptions that drive the entire model: the annual contribution, the contribution escalation rate, assumed interest earnings, and an inflation index. On the right, the model rolls forward year by year with an opening balance, contributions, expenditures, and a closing balance.

The danger is not reading any one cell. It is judging whether the whole picture holds together. A study can look perfectly healthy on the surface while quietly relying on optimistic assumptions, an aggressive contribution-escalation rate, a low inflation index, or a deferred major project that lands the year after you buy. Spotting that takes someone who has read hundreds of these and knows where the soft spots hide. For most buyers, this single document is the strongest argument against going it alone.

"Can't I just ask ChatGPT or Gemini?"

It is a fair question, and increasingly a common one. If the documents are dense, why not upload them to a general AI chatbot and ask it to summarize the risks?

Because there is a world of difference between a tool that can pull numbers and a tool that pulls the right numbers. We have watched people drop a document package into a general assistant, ask it questions in a Google Drive, and get back an answer that sounded authoritative and was simply wrong, citing the wrong reserve balance, mixing up the operating and reserve funds, or reading a figure from the wrong year. The output reads beautifully. It is also confidently incorrect.

That is the real trap. A general-purpose model is built to sound fluent, not to be right about a specific reserve fund study. On a table like the one above, with dozens of components, phased projects, and stacked financial assumptions, a small misread produces a clean paragraph that hides a five-figure error. With dense financial documents, a convincing wrong answer is more dangerous than no answer at all, because it talks you out of the very caution that would have protected you.

And then there is recourse. If a free chatbot gets it wrong and you remove conditions based on its summary, who is accountable? No one. There is no expert who reviewed it, no guarantee, and no one to call when the special assessment notice arrives.

This is exactly the gap CondoScan is built to close. We do not run your documents through a general chatbot. We use a state-of-the-art analysis fine-tuned specifically for condo documents, then a human expert team reviews the findings before anything reaches you, and we back the work with a money-back guarantee. You get the speed of technology with the accuracy and accountability that a six-figure decision deserves.

The deadline problem

Even an experienced reader faces a structural problem: time. In a typical Alberta purchase, you have a short window to review documents and remove your conditions. That is rarely enough time to read hundreds of pages thoroughly, cross-reference the reserve fund against the financials, and trace issues through years of minutes, especially while you are also juggling financing, inspections, and your day job.

Deadline pressure is precisely when important details slip through. The documents you most need to read slowly are the ones you end up skimming fastest.

The true cost of getting it wrong

Consider the math. A professional review costs a few hundred dollars. A special assessment for a major repair, balcony remediation, a new roof, parkade work, can run from a few thousand dollars to well over $20,000 per unit. If you remove conditions without spotting the warning signs, that bill becomes yours, even if the underlying problem started long before you owned the unit.

Framed that way, a review is not really an expense. It is inexpensive insurance against a low-probability, high-cost mistake, plus the leverage to renegotiate or walk away if the documents reveal something serious.

A quick self-check before you DIY

DIY can be reasonable if you can honestly answer yes to all of these:

- I have a background in property management, accounting, or condo governance.

- I have several uninterrupted hours before my condition deadline.

- I know how to judge whether a reserve fund is adequately funded for this building.

- I am confident reading multiple years of minutes to trace unresolved issues.

- I understand condo insurance certificates and deductible exposure.

If any of those is a no, the risk of a costly miss is real.

When a professional review pays off

You should always read your condo documents; nobody cares about your purchase more than you do. But for most buyers, the math is simple. A professional review gives you a clear, written assessment of the risks and the confidence to act, all for a fraction of what a single missed problem would cost.

This is where CondoScan helps. We combine technology-powered analysis with an expert team to deliver a clear report, typically within 24 hours, and we are available to answer your questions before your condition deadline. When you are ready to compare providers, see how to choose a condo document reviewer in Calgary. You still make the decision. We just make sure you are making it with the full picture.

Frequently asked questions

Can I review condo documents myself?

You can, and you should always read them. But interpreting reserve fund studies, financial statements, bylaws and years of meeting minutes well enough to catch a looming special assessment takes experience. Most buyers don't have the time or background to do this confidently within a condition-removal deadline.

What do buyers most often miss when reviewing condo documents themselves?

The most common misses are an underfunded reserve fund relative to its study, early signals of an upcoming special levy buried in meeting minutes, restrictive bylaws (such as rental or pet limits), and insurance deductibles that owners could be responsible for.

Is a professional condo document review worth it?

For a purchase worth hundreds of thousands of dollars, a few hundred dollars for a professional review is inexpensive insurance. A single missed special assessment can cost far more than the review itself, and a clear report helps you negotiate or walk away with confidence.

Can I just use ChatGPT or Gemini to review my condo documents?

General-purpose AI tools can extract numbers, but they are built to sound fluent, not to be reliably correct about a specific reserve fund study. We have seen them pull the wrong reserve balance or read a figure from the wrong year while sounding completely convincing, and if a free chatbot gets it wrong you have no expert review, no guarantee, and no recourse. CondoScan instead uses analysis fine-tuned specifically for condo documents, backed by a human expert team and a money-back guarantee.

Related reading

June 19, 2026

How to Choose a Condo Document Reviewer in Calgary

An honest 2026 buyer's guide to turnaround, pricing, expertise, and the questions that actually matter, with a side-by-side look at the major Alberta providers.

July 10, 2026

Condo Document Review in Edmonton: A Buyer's Guide (2026)

Same Condominium Property Act, different buildings. Here is what Edmonton condo buyers need to know about reviewing documents before removing conditions, from ICE District towers to walk-ups in Oliver and complexes in St. Albert and Sherwood Park.

July 3, 2026

How Much Does a Condo Document Review Cost in Alberta? (2026 Price Guide)

A transparent, up-to-date look at what condo document reviewers actually charge across Calgary, Edmonton, and the rest of Alberta, with a side-by-side price comparison and the one number that matters more than price: turnaround.